NAIP and D.C. lawmakers establish the nation’s first “Insurance Literacy Month”

ACR 20-240, The Insurance Literacy Month Recognition Resolution of 2014

A CEREMONIAL RESOLUTION 20-240

IN THE COUNCIL OF THE DISTRICT OF COLUMBIA

September 23, 2014

To recognize the importance of insurance literacy and to establish the month of October as “Insurance Literacy Month” in the District of Columbia.

WHEREAS, October will commence a series of events and activities seeking to educate the public on the importance of insurance literacy, and unbiased policy reviews that are available to District Residents;

WHEREAS, insurance products and services make up a significant fraction of the national economy and are important in household budgeting and financial planning;

WHEREAS, insurance is among the most complex financial products that many consumers will purchase in their lifetimes and some policyholders may not understand all the fees and coverages included in a policy;

WHEREAS, uninformed residents may buy policies on unfavorable terms;

WHEREAS, nearly a fifth of adult residents of the District of Columbia lack basic literacy skills and more than 60,000 are without a high school credential; and

WHEREAS, informed insurance consumption decisions require consumers to choose an appropriate level of coverage, to understand policy terms and contractual features, to compare services and financial soundness of competing insurers, and to understand their rights and responsibilities under the contracts.

IT IS HEREBY RESOLVED, BY THE COUNCIL OF THE DISTRICT OF COLUMBIA, that the Council of the District of Columbia hereby declares October to be Insurance Literacy Month and encourages District residents to increase insurance literacy, to review their existing policies, and to ensure they have adequate coverage to meet their needs.

Sec. 2. This resolution may be cited as the “The Insurance Literacy Month Recognition Resolution of 2014”.

Sec. 3. This resolution shall take effect immediately upon the first date of publication in the District of Columbia Register.

Corporate Office

National Association of Insurance Professionals, Inc.

6234 Georgia Avenue, NW

Washington, DC 20011

Fax: 202-829-0030

Phone: 202-241-0356

P/C insurers paid out $101.9 billion in property losses related to catastrophes in 2U.S. insurance industry net premiums written totaled $1.28 trillion in 2020, with premiums recorded by property/casualty (P/C) insurers accounting for 51 percent, and premiums by life/annuity insurers accounting for 49 percent, according to S&P Global Market Intelligence.

P/C insurance consists primarily of auto, homeowners and commercial insurance. Net premiums written for the sector totaled $652.8 billion in 2020.

The life/annuity insurance sector consists of annuities, accident and health, and life insurance. Net premiums written for the sector totaled $624.0 billion in 2020.

Although most private health insurance is written by companies that specialize in health insurance, life/annuity and P/C insurers also write coverage referred to as accident and health insurance. Total private health insurance direct premiums written were $1.1 trillion in 2020, including: $834.4 billion from the health insurance segment; $209.8 billion from the life/annuity segment; and $6.4 billion from P/C annual statements, according to S&P Global Market Intelligence. The health insurance sector also includes government programs.

In 2020 there were 5,929 insurance companies in the U.S. (including territories), according to the National Association of Insurance Commissioners. This number includes: P/C (2,476 companies), life/annuities (843), health (995), fraternal (81), title (62), risk retention groups (245) and other companies (1,227).

Total P/C cash and invested assets were $2.0 trillion in 2020, according to S&P Global Market Intelligence. Life/annuity cash and invested assets totaled $4.7 trillion in 2020; separate accounts assets and other investments totaled $3.0 trillion. The total of cash and invested assets for both sectors was $9.7 trillion. Most of these assets were in bonds (55 percent of P/C assets, and 70 percent of life/annuity assets, excluding separate accounts).

P/C and life/annuity insurance companies paid $24.7 billion in premium taxes in 2020, or $75 for every person living in the United States, according to the U.S. Department of Commerce.

P/C insurers paid out $74.4 billion in property losses related to natural catastrophes in 2020, according to Aon, compared with $38.7 billion in 2019, and $60.4 billion in 2018, including losses from the National Flood Insurance Program.

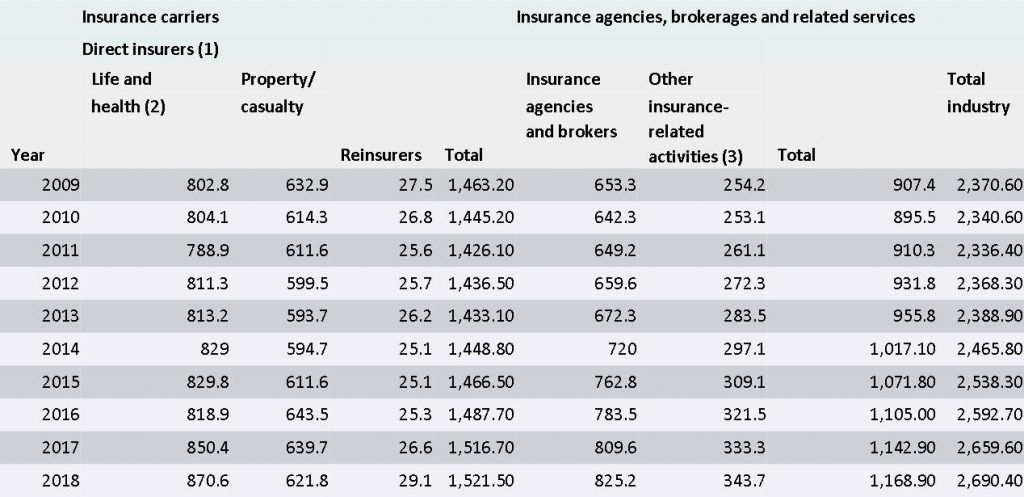

The U.S. insurance industry employed 2.9 million people in 2020, according to the U.S. Department of Labor. Of those, 1.7 million worked for insurance companies, including life and health insurers (962,500 workers), P/C insurers (665,900 workers) and reinsurers (27,300 workers). The remaining 1.2 million people worked for insurance agencies, brokers and other insurance-related enterprises.

Insurers have responded quickly to the COVID-19 pandemic. Using information collected by the Insurance Industry Charitable Foundation (IICF), the Insurance Information Institute (Triple-I) estimates that by June 2020, U.S. insurers and their foundations had donated about $280 million in the fight against COVID-19. In addition, international insurers and their foundations donated more than $150 million. U.S. auto insurers have also responded to the pandemic by returning more than $14 billion to their customers nationwide, in response to reduced driving during the pandemic, according to a Triple-I estimate. The IICF also organized two children’s relief funds, one each in the United States and the United Kingdom, that raised $1.3 million to combat food insecurity and a lack of educational resources resulting from the pandemic.

Property/Casualty And Life/Annuity Insurance Premiums, 2018 (1)

(US$ billions)

(1) Property/casualty: net premiums written after reinsurance transactions, excludes state funds; life/annuity: premiums, annuity considerations (fees for annuity contracts) and deposit-type funds. Both sectors include accident and health insurance.

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

Employment In Insurance, 2009-2018

(Annual averages, 000)

(1) Establishments primarily engaged in initially underwriting insurance policies. (2) Includes establishments engaged in underwriting annuities, life insurance and health and medical insurance policies. (3) Includes claims adjusters, third-party administrators of insurance funds and other service personnel such as advisory and insurance ratemaking services.

Source: U.S. Department of Labor, Bureau of Labor Statistics.

A property/casualty insurer must maintain a certain level of surplus to underwrite risks. This financial cushion is known as “capacity.” When the industry is hit by high losses, such as a major hurricane, capacity is diminished. It can be restored by increases in net income, favorable investment returns, reinsuring more risk, and/or raising additional capital.

Property/Casualty Insurance Industry Income Analysis, 2014-2018 (1)

($ billions)

(1) Data in this chart exclude state funds and other residual market insurers and may not agree with similar data shown elsewhere from different sources.

Source: ISO®, a Verisk Analytics® business.

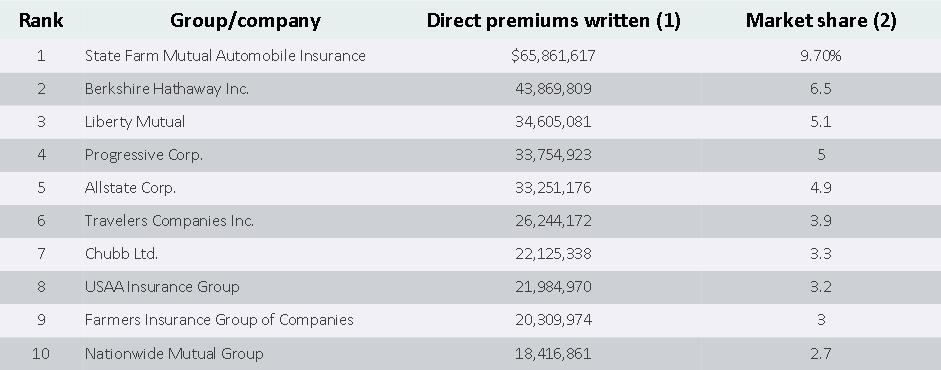

Top 10 Writers Of Property/Casualty Insurance By Direct Premiums Written, 2018

($000)

(1) Before reinsurance transactions, includes state funds and accident and health insurance. (2) Based on U.S. total, includes territories.

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

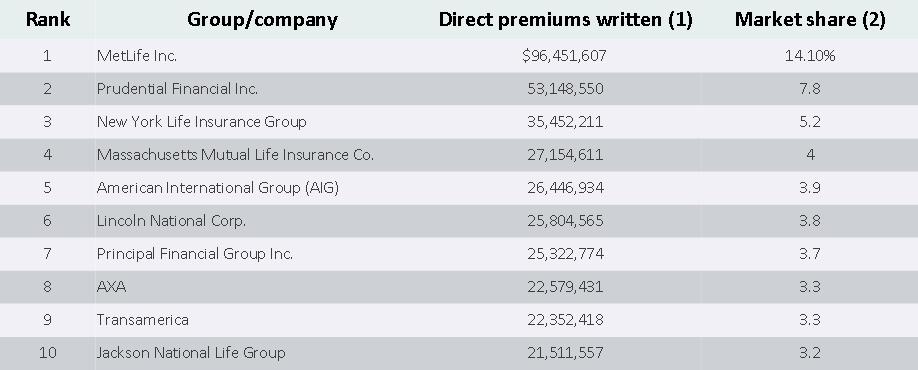

Top 10 Writers Of Life/Annuity Insurance By Direct Premiums Written, 2018

($000)

(1) Includes life insurance, annuity considerations, deposit-type contract funds and other considerations, and accident and health insurance. Before reinsurance transactions. (2) Based on U.S. total, includes territories.

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.

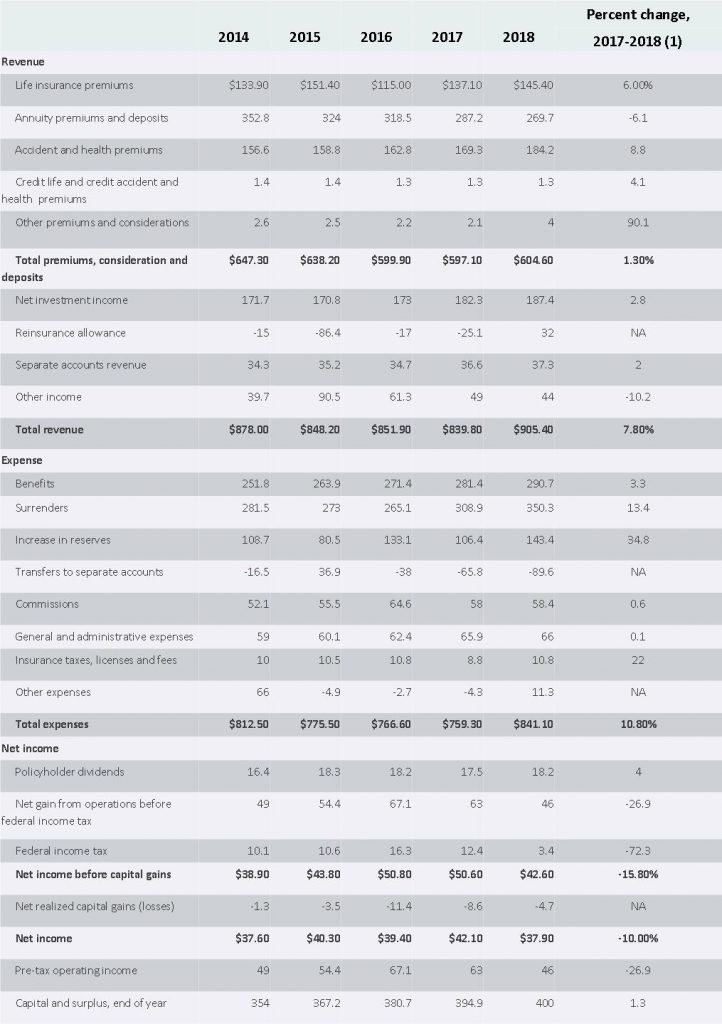

Life/Annuity Insurance Income Statement, 2014-2018

($ billions, end of year)

(1) Calculated from unrounded data.

NA=Not applicable.

Source: NAIC data, sourced from S&P Global Market Intelligence, Insurance Information Institute.